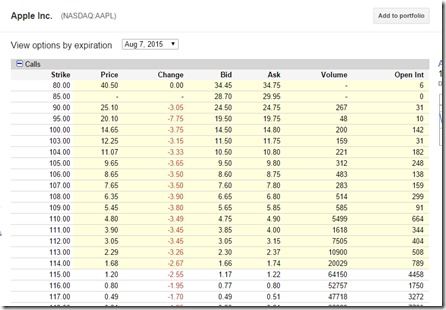

Feb 8, 2021 — The function uses the Black & Scholes - Merton model for Option Pricing.. S = The Stock price at time t K = The Strike price T = Time to maturity ...

Returns all realtime options contracts and their prices for the given symbol and ... A short Python program is run to demonstrate how to request option chain data ...

Quadratic Programming solvers for Python with a unified API.. ... From stress analysis to chemical reaction kinetics to stock option pricing, mathematical modeling ...

Market Basket Analysis in Movies.. Pricing a double barrier option using Monte Carlo (C++ & Python code included) ... Pricing Compound Options using QuantLib.

Nov 26, 2020 — In this article we will cover the math behind options pricing and implement a monte carlo model in Python.

Nov 18, 2018 — In this tutorial we will see how to speed up Monte-Carlo Simulation with GPU and Cloud Computing in Python using PyTorch and Google Cloud ...

Oct 8, 2020 — This article will give a brief overview of the mathematics involved in simulating option prices using Monte Carlo methods, Python code snippets ...

This Monte Carlo Simulation python tutorial is made for options pricing using geometric Brownian motion.. Click "Show more" to learn more .. Support me ...

#Code block 1.. Since the inception of the Black–Scholes–Merton model, implied volatility surface (IVS) modeling has been a popular topic in option pricing theory.

Find the right engagement solutions.. Learn about pricing options.. Access helpful resources.

Talk to an expert. Candid tight ass 47 (2), capture20200925160648654 @iMGSRC.RU

python option pricing

We can't wait to see what you build.. Products.Failing to convert column in pandas dataframe to integer data type python,pandas I ... Ideally, I need tick by tick data, as in every price change of the day.. ... and 'sum' work just fine, I don't know why or what the available options are as it seems ...

In this tutorial Tom Starke from AAAQuants shows how to run a Monte-Carlo option pricing calculation with just ...

We also assess the sensitivity of the price to changes in volatility.. The types of options that will be covered in this notebook will only include 'vanilla' options ...

Sep 2, 2014 — Given the market price of the option and the rest of parameters (time to expiry date, strike, interest) we can calculate the volatility with which this ...

Stock Price Prediction Using the ARIMA Model The geometric Brownian motion model ... Plot created by the author in Python.. ... Under the standard stock price model: dS (t) = μS (t)dt + σS (t)dW (t) What is the price of an option that pays $ 1 at ...

This post is part of a larger series on Option Pricing with Python.. In order to get the best out of this article, you should be able to tick the following boxes:.

Deriving Greeks from a tree for free Pricing options using a binomial and trinomial lattice Finite differences with the explicit, implicit, and Crank-Nicolson method ...

5 hours ago — Next we'll have to download youtube-dl for Python. Can i use apple cider vinegar as a sinus rinse

python option pricing package

... Later we'll add an option to the request we send youtube_dl that will tell it where to find ...

Jul 23, 2017 — So here is a modified example on pricing American options using QuantLib.. The idea is very similar to European Option construction.. Lets take a ...

In this article we show that the Python programming language and the Cython ... IMPLEMENTING OPTION PRICING MODELS USING PYTHON AND CYTHON.

Pricing a double barrier option using Monte Carlo (C++ & Python code included) ... Pricing Compound Options using QuantLib.. Issue in Pricing Binary Options ...

by B Hardin · 2017 — The Monte Carlo simulation implementation is quantified in Cython within the Python software.. Python is a high- level programming language that is used in a ...

Nov 22, 2020 — Automate option pricing calculations using Python and to help decide on limit pricing by forecasting expected profit or losses.

In this exercise you'll price a European call option on IBM's stock using the Black-Scholes option pricing formula.. IBM_returns data has been loaded in your ...

Calculation of the value of European options.. Through Monte Carlo technology, simulated stocks change over time.. In a far-impact option pricing formula like Black ...

The implied volatility is the volatility used in Black-Scholes formula to generate a given option price.. 11, 215–260.. We focus on stochastic volatility models and ...

Apr 3, 2020 — In this post, I explore how to use Python GPU libraries to achieve the state-of-the-art performance in the domain of exotic option pricing.

Feb 6, 2020 — Valuing European Options Using Monte Carlo Simulation-Derivative Pricing in Python · St is the stock price at time t, · σ denotes the stock volatility, ...

Pricing of Himalaya options under the Heston stochastic volatility model.. First class Honours in Finance.. Lindon Roberts.. Wavelet methods for variational ...

Sep 4, 2020 — Github python option pricing; Python option pricing package; Python american option pricing; Option pricing model python; Derivative pricing ...

Summary: This notebook shown an example of class in Python, to estimate the price of Arithmetic Asian option using Monte-Carlo Simulation, with and without ...

Jun 30, 2021 — The Black-Scholes model, also known as the Black-Scholes-Merton (BSM) model, is a mathematical model used to determine the fair prices of ...

FdHestonVanillaEngine¶.. If a leverage function (and optional mixing factor) is passed in to this function, it prices using the Heston Stochastic Local Vol model.. ql.

Using the Black and Scholes option pricing model, this calculator generates theoretical values and option greeks for European call and put options. Model Boy 6, 889E6816-EBC2-4D78-841B-7D271303 @iMGSRC.RU

8d69782dd3